Bitcoin keeps testing the supporting level of 19000 without breaking it. Bitcoin is still likely to pull away from the support and target the level of 22000 next.Having formed the new minimum, gold is trying to recover. So far, this asset is likely to approach the level of 1735, which is located next to the downtrend and broken downtrend denoted by the blue line on the monthly chart. Gold might potentially pull from the crossing point of these trendlines and drop.American stock index S&P 500 has pulled away from the supporting level of 3639.00. The asset was trying to close the trading day by engulfing and thus signifying the potential growth. However, should the asset head north, it might have to face the broken local uptrend denoted by points 1 and 2 on the chart below.

from Tickmill Expert Blog - Forex Traders Blog https://www.tickmill.com/blog/bitcoin-and-sp500-are-on-the-rise"

via IFTTT

Thursday, September 29, 2022

Wednesday, September 28, 2022

How the mini-Budget tax cuts will affect you

Chancellor Kwasi Kwarteng's mini-Budget was full of tax cuts that will change your take-home pay

from Moneyweek RSS Feed https://moneyweek.com/personal-finance/tax/605376/how-the-mini-budget-tax-cuts-will-affect-you

via IFTTT

from Moneyweek RSS Feed https://moneyweek.com/personal-finance/tax/605376/how-the-mini-budget-tax-cuts-will-affect-you

via IFTTT

3 funds to invest in Japanese value stocks

Japanese stocks have fallen out of favour with investors, but they are looking ripe for recovery, says Max King.

from Moneyweek RSS Feed https://moneyweek.com/investments/stockmarkets/japan-stockmarkets/605379/3-funds-offering-value-in-japanese-stocks

via IFTTT

from Moneyweek RSS Feed https://moneyweek.com/investments/stockmarkets/japan-stockmarkets/605379/3-funds-offering-value-in-japanese-stocks

via IFTTT

Live Analysis | 28th September 2022

Haven demand is helping boost Treasuries amid worries over a financial crisis in the UK, exacerbated by the BoE’s decision to purchase longer dated Gilts. The further dive in equities is adding to the flow into Treasuries. The market was also looking oversold.

The front end of the curve is outperforming in a classic move with the 2-year yield down 16 bps at 4.125%. Yesterday’s richening broke a record string of 13 straight sessions of higher rates. The 7-year is down 9.5 bps to 3.995%. The 10-year has richened 6.5 bps to 3.880% after testing 3.99% Tuesday. It has not closed with a 4-handle since December 2007. The bond is down 2 bps to 3.806%. The traditional haven, gold, is also firmer, up 0.38% to $1635.

Meanwhile, Wall Street has bounced from earlier losses and is mixed. The US30 future is up 0.47%, with the S&P 0.27% higher, while the US100 is down -0.11%. The USDIndex has been all over the board, though inside a relatively narrow range. Currently it is at 114.259, heading back toward the 114.08 low, having slide from the intraday peak of 114.778. Along with the tumult in the UK, the buck benefited from news out of the White House that suggested there would be no currency agreement to cap the ascent of the greenback.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

from HF Analysis /520202/

via IFTTT

GBP Stabilises Following Sharp Losses As IMF Criticises UK Tax-Cuts

GBP Finds Equilibrium - For Now Following the heavy volatility we saw in GBP on Friday and Monday, price action has since stabilised. In GBPUSD in particular, price plunged almost 5% on Monday before reversing around 70% of those losses. The market has since been underpinned by support at the 1.0646 level though looks vulnerable to further losses. In terms of deciphering the bounce off the lows, the move looks be mainly linked to large players simply looking to buy GBP at record lows. There have been reports of many sizeable players looking to secure GBP purchases given how far below its 5-year average it has fallen, and therefore not particularly indicative of the view that the currency is likely to recover near-term.Adverse Market Reaction To Mini-BudgetThe driver behind the fall itself was the market reaction to the mini-budget announced by the UK government on Friday. Chancellor Kwasi Kwarteng announced the removal of the highest 45% tax bracket in the UK, a reduction in stamp duty and a 1% reduction in income tax. Additionally, Kwarteng announced that the planned 1.25% increase in National Insurance tax will be scrapped.Looking at corporates then, Kwarteng removed the cap on bankers’ bonuses, put in place after the GFC, and has scrapped next year’s planned increase in corporation tax from 19% to 25%. In all, the new tax cuts would, according to the budget, be funded by fresh borrowing of £45 billion by the UK government.With GBP seeing its third worst day behind the COVID outbreak and Brexit referendum results, the market’s verdict on the “pro-growth” measures are quite clear. Critics have called the moves a disaster for the UK economy stating that the measures will simply add to the inflationary spiral currently gripping the UK, forcing the BOE to tighten more aggressively.BOE In Focus Indeed, with GBP sinking to record lows against USD, speculation of an emergency BOE rate-hike was rife on Monday. However, the BOE issued a statement saying that while it was monitoring the situation and did indeed have tools, and the willingness to use them, at its disposal, it would wait until the next scheduled BOE meeting in November to take action.IMF Criticises UK Tax-CutsThe IMF this week joined those criticising the UK government. The fund labelled the tax cuts excessive and urged a review of the measures, specifically those aimed at helping the highest earners in the UK. The IMF warned that the untargeted tax cuts would likely lead to greater inequality in the UK and would undermine monetary policy.In response to the situation, new PM Truss announced that the government would issue a statement on November 23rd adding further details to the budget and setting out a full fiscal plan. In the meantime, the new chancellor is undertaking meetings with investment banks aimed at gathering information ahead of that date.Technical ViewsGBPUSDThe market is trading almost a thousand pips below where it was last week. The break below the 1.1474 level is a major bearish development and while below there, the focus is on a further push lower. However, while the prior 1985 lows at 1.0539 hold, we are likely to see a period of range-bound activity while the market awaits fresh drivers.

from Tickmill Expert Blog - Forex Traders Blog https://www.tickmill.com/blog/gbp-stabilises-following-sharp-losses-as-imf-criticises-uk-tax-cuts"

via IFTTT

from Tickmill Expert Blog - Forex Traders Blog https://www.tickmill.com/blog/gbp-stabilises-following-sharp-losses-as-imf-criticises-uk-tax-cuts"

via IFTTT

Hundreds of mortgage products withdrawn as interest rates surge

Hundreds of mortgage products have been withdrawn after sterling crashed to the lowest levels in decades against the dollar and the Bank of England said it wouldn’t hesitate to step in and raise interest rates further.

from Moneyweek RSS Feed https://moneyweek.com/personal-finance/mortgages/605372/hundreds-of-mortgage-products-withdrawn-as-interest-rates-surge

via IFTTT

from Moneyweek RSS Feed https://moneyweek.com/personal-finance/mortgages/605372/hundreds-of-mortgage-products-withdrawn-as-interest-rates-surge

via IFTTT

Investment Bank Outlook 28-09-2022

BNY MellonReserve Import Cover Shows VulnerabilityAlthough August macro data for APAC countries in general showed continued deterioration, one relative bright spot was tentative signs of stabilization in economic conditions in China. Aside from declining credit growth (aggregate financing eased 0.2ppt to 10.5%), China's activity data otherwise was encouraging. Examples of recovery signs came from fixed asset investment (5.8% y/y, +0.1ppt), industrial production (3.6% y/y ytd, +0.1ppt), and infrastructure investment (8.3% y/y ytd, +0.9ppt). And the year-to-date growth rate in retail sales was back in positive territory. The biggest drag on China's economy, however, remains the property sector. Property investment declined further, to -7.4% (-1.0ppt), and average home prices across 70 cities dropped for a twelfth consecutive month (-2.1% y/y in August).Given ongoing efforts to ensure the implementation of policy measures already announced, we believe that China's underlying economic fundamentals should be able to withstand the complicated global environment – slowing growth momentum, aggressive tightening of monetary policies, substantial volatility in asset markets, etc.Slowing external conditions, reflected particularly in falling exports growth, along with domestic growth recoveries and high commodity prices (elevated import growth) have continued to exert severe stress on APAC trade balances. As discussed previously (here), the exports shock is an increasing concern. India's exports in August grew 1.6% y/y while imports surged 37.3% y/y. Likewise, South Korea: exports up 6.6% y/y while imports jumped 28.2% y/y. The Philippines' exports in July fell 4.2% y/y against imports rising 21.5% y/y. The repricing of global assets since the Federal Reserve's policy meeting last week has been significant. Alongside the market recalibrating a higher Fed terminal rate, the 2y US Treasury yield has spiked over 20bp since the meeting (up 75bp on the month) to around 4.30%. Aggressive tightening of Fed policy raises risks of a growth slowdown, which, in turn, exerts downside pressure on equity and bond prices. EM and APAC FX have additionally suffered on concerns around capital outflows. The chart and table below show APAC asset price changes since the beginning of the month, as well as FX volatilities in the region.FX volatility plays a key role in the stability of financial markets across APAC. A weak currency would not only raise the prospect of inflationary pressure in the medium term but also, and crucially, run the spillover risk of triggering capital outflows from other assets.

from Tickmill Expert Blog - Forex Traders Blog https://www.tickmill.com/blog/investment-bank-outlook-28-09-2022"

via IFTTT

from Tickmill Expert Blog - Forex Traders Blog https://www.tickmill.com/blog/investment-bank-outlook-28-09-2022"

via IFTTT

EURGBP pivots around the key 0.9000 level

Bank of England Chief Economist Huw Pill stated that the BOE is ready to make a strong policy response at its November 3 policy meeting, in a bid to calm the battered UK bond market and Sterling. The comments helped prop up Sterling and saw it recover from record lows against the Dollar and Euro, which were hit during Monday’s massive sell-off.

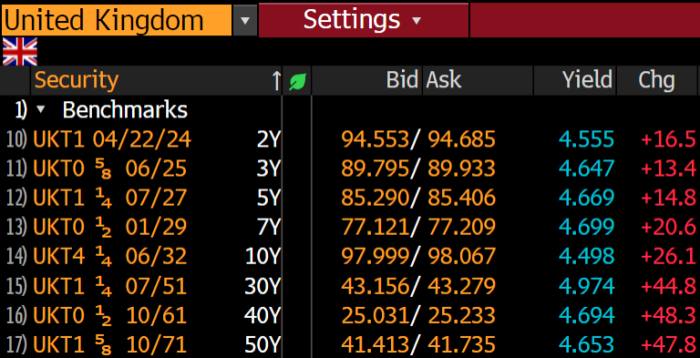

As investors demand higher compensation for holding on to UK government debt, the recent decline in the value of the Pound has been accompanied by an increase in UK bond yields. The yield on the 10-year gilt on Tuesday hit an almost 14-year high of 4.537%. This demand comes in response to last Friday’s tax cut announcement from Chancellor Kwasi Kwarteng.

There are growing fears that the world economy will enter a recession, amid tax cuts and guarantees that billions of pounds of energy prices will be paid for by issuing more debt.

The BOE is committed to bringing inflation back to 2.0% and will raise interest rates to slow the economy down. In light of rising inflation expectations, the market is now pricing in a 200bp hike over the rest of 2022.

Meanwhile, the EURGBP exchange rate remains vulnerable amidst a deteriorating global backdrop largely a result of rising US interest rates. Rising interest rates have increased the cost of money globally, reducing borrowing and economic activity. Falling stock markets and commodity prices are evidence of this slowdown, as is the soaring US Dollar. This unhelpful backdrop is likely to keep UK assets under pressure and Sterling will struggle longer.

EURGBP’s intraday bias remains neutral at the moment. The latest rally to 0.90 area turn the 0.8720 resistance into support. A move above 0.9250 will target the 0.9500 long term resistance. However, a break of the 0.8270 support will cloud the near-term outlook. For now, trading within the range is likely to remain in force and the 0.9000 round figure mark will be the middle price traders are watching.

Click here to access our Economic Calendar

Ady Phangestu

Market Analyst – HF Educational Office – Indonesia

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

from HF Analysis /520089/

via IFTTT

Weekly Market Update: 27 September 2022

U.S Dollar heads into the new week renewing 20-year highs.

Dollar

The Dollar begins the week on the front foot, refreshing its 20-year highs as risk aversion intensifies in the global markets. Key drivers thus far have been comments from various FED members, which indicate their proclivity towards maintaining their hawkish stance to keep fighting record high inflation. Other key elements adding to the risk aversion is the increasing realisation from other central banks around the world, that they might need to take some action to defend their respective currencies from a rampant Dollar.

Technical Analysis (H4)

In terms of market structure, price action printed out a bullish continuation pattern in the form of a bull flag around the 109.00 range and subsequently printed out an impulsive wave. Current price action is locked in a range between the 113.06–114.30 area, where a significant break above will see bulls continue to drive price, or a break below will give sellers an opportunity to test the 111.00 area.

Euro

The Euro kicks off the week under significant pressure as it attempts to pull back from fresh 20-year lows. The renewed buying interest can be attributed to the latest hawkish comments coming from ECB officials as well as Christine Lagarde saying, “we expect to raise interest rates further over the next several meetings”. Additionally, the prospect of easing the energy crisis in the bloc with a delay on the proposed price caps of Russian oil imports has relieved some of the pressure on the currency as hopes of a stable energy plan take centre stage. Going forward key drivers will continue to be the divergence between the FED and ECB as well as geopolitical effervescence and macroeconomic data.

Technical Analysis (H4)

In terms of market structure, price action printed out a bearish continuation pattern in the form of a bear flag around the 1.00 range and subsequently printed out an impulsive wave to the downside. Current price action is locked in a range between the 0.970–0.955 area, where a significant break above will see bulls challenge the 0.948 area, or a break below will give sellers an opportunity to drive price even further down.

Pound

Sterling begins the week rebounding from record lows amid fears of a “mismanagement of the UK economy” under the newly formed Tory government. The fears are centred around proposed tax cuts as well as a new energy bill which could potentially increase the rate of inflation and general debt incurred by the government. With that being said, there are speculations of an emergency rate hike by the BoE to alleviate some of the pressure on the currency, and investors have priced in roughly 175 basis points of hikes by November.

Technical Analysis (H4)

In terms of market structure, price has been in a downtrend, printing bearish continuation patterns to the downside with lower-lows and lower-highs. Current price action is locked in a range between the 1.093–1.033 area, where a break below will see sellers continue to drive price potentially towards parity, conversely a break above will put buyers in line to challenge the 1.134 area.

Gold

Gold heads into the new week bouncing from a 29-month low as investors eye the pullback from the Dollar. The yellow metal remains bearish as investors await comments from FED chairman Jerome Powell as well as data in the form of Consumer confidence for the month of September for further fundamental impetus.

Technical Analysis (H4)

In terms of market structure, price action has confirmed the formation of the bear flag that formed around the $1 672 range by yielding an impulsive wave to the downside. Henceforth, buyers could retest the lows of the broken pattern around the $1 660 area or bears could continue the path of least resistance and keep moving price southbound

from HF Analysis /520153/

via IFTTT

Daily Market Outlook, September 28, 2022

Daily Market Outlook, September 28, 2022 Overnight Headlines Moody's Warns UK Unfunded Tax Cuts Are 'Credit Negative' IMF Tells UK To Re-Evaluate Tax Cut As Global Criticism Mounts UK Price Inflation In Shops Hits Record High As Pound Tumbles Treasury 10-Year Yields Rise Above 4% In First Time Since 2010 Poll: Fed To Take Rates Even Higher With Further Pain Ahead Fed’s Kashkari Says Rate-Hike Pace Appropriate To Cool Prices White House’s Deese Doesn’t See Another Plaza Accord Ahead White House Mulling Potential Yellen Departure After Midterms Senate Advances US Funding After Manchin Drops Energy Bid BoJ Board Agreed On Need For Vigilance On Sharp Yen Moves Putin Raises Gas Pressure As Moves To Annex Ukraine Regions EU Warns Against Attacks On 'Active Infrastructure' After Leaks Apple Ditches iPhone Production Increase After Demand Falters China's Offshore Yuan Hits Record Low Against Strengthening Dollar Oil Tumbles As Dollar Hits Record In Fresh Blow To Commodities US Futures Fall After S&P 500 Hits New Low For The YearThe Day Ahead Asian equity markets came under renewed pressure and the US dollar strengthened against other major currencies. Treasury yields climbed further after hawkish Fed comments and some strong US data including a rise in consumer confidence. The White House also reportedly played down prospects of a 1985 Plaza-type agreement to weaken the dollar. Regarding the UK, the IMF said fiscal policy should not “work at cross purposes to monetary policy”. Data from the British Retail Consortium showed another record rise in shop prices in September. In the absence of significant economic data releases, especially in Europe and the UK, the focus will remain on several central bank speakers today. In the UK, yesterday saw comments from BoE MPC member and Chief Economist Huw Pill who said there will be a “significant monetary policy response” to recent developments. Fellow rate-setters Deputy Governor Jon Cunliffe and new external MPC member Swati Dhingra are due to speak today. The BoE’s Cunliffe will speak on payment systems rather than the economic or monetary policy outlook. This evening, Dhingra will chair a panel with Chicago Fed President Charles Evans on inflation and monetary policy. Dhingra dissented at her first policy vote last week in favour of a smaller 25bp hike, rather than the majority 50bp, putting her at the most dovish end of the spectrum. There are also several scheduled ECB and US Fed speakers today as well, as the two central banks prepare to increase interest rates further in response to high inflation. Ahead of this Friday’s Eurozone flash CPI inflation figures, which are expected to show a rise to a record high, ECB President Lagarde will participate in a ‘keynote fireside chat’ this morning. Fed Chair Powell will also give welcome remarks at an event today. US advance trade data and pending home sales will draw some attention in the afternoon session. The goods deficit is forecast to narrow slightly, while pending home sales are expected to fall as rising interest rates dampen housing activity.FX Options Expiring 10am New York Cut EUR/USD: 0.9650 (302M), 0.9725-30 (444M) USD/JPY: 143.40-50 ( (431M), 143.94-00 (263M), 145.00 (554M) EUR/JPY: 138.00 (401M). USD/CHF: 0.9890-00 (830M) AUD/USD: 0.6285 (200M, 0.6495-05 (594M) USD/CAD: 1.3760-65 (1.28BLN)Technical & Trade ViewsEURUSD Bias: Bearish below 1.00 Under pressure as USD buying picks up steam in Asia EUR/USD down 0.45% as USD bid across the board - led by GBP/USD Equities pressured as negative feedback loop between USD and equities bites US 10-year yield testing yesterday's 3.9930% high and underpinning USD E-minis down 0.45% while AXJ equity index down over 1.5% EUR/USD below Tuesday's 0.9570 low with support at Monday's 0.9528 low Bids are tipped ahead of 0.9500 with talk of stops below 20 Day VWAP bearish, 5 Day bearishGBPUSD Bias: Bearish below 1.10 Heavy, scepticism on UK pro growth policies resurfaces Off 0.5% as sterling sellers return, with EUR/GBP up 0.2% White House's Deese - UK economic plans need 'fiscal prudence' Moody's warns UK unfunded tax cuts are 'credit negative' Headlines underline markets scepticism with UK's pro growth mini budget Tuesday's 1.0650 low and early Asian 1.0737 top initial support, resistance 20 Day VWAP is bearish, 5 Day bearishUSDJPY Bias: Bullish above 140 Yen shows broad strength, as risk appetite sours Risk off in Asia, in response to surging yields on Tuesday in EZ and U.S. Nikkei -1.85%, AsiaxJP stocks -1.4% and E-mini S&P futures -0.55% Yen shows broad strength, as Japanese investors repatriate USD/JPY -0.1%, EUR/JPY -0.5%, GBP/JPY -0.75% and AUD/JPY -0.8% Pivotal 141.03 now major support Psychological 145.00 first resistance, then pre intervention 145.90 high London 144.06 low, then 143.10 initial supports 20 Day VWAP is bullish, 5 Day bullishAUDUSD Bias: Bearish below .6750 New low as USD firms – muted reaction to better Aus data AUD/USD eased to 0.6411 before Aus retail sales better than expected It is the lowest traded since May 2020 - as yesterday's low was 0.6413 Muted reaction to the better retail sales as USD broadly firmer in Asia AUD/USD looks vulnerable after clearly breaking important fib at 0.6463 There isn't much in the way of support until weekly lows at 0.6235/50 20 Day VWAP is bearish, 5 Day bearishBTCUSD Bias: Bearish below 25.3K BTC gave up a +5% gain to close negative and sub 19k on the day BTC is still down ~58.5% so far this year CFTC - BTC specs +451 contracts, long rises to 577 contracts; BTC -6.23% in period Crypto Exchange FTX President Brett Harrison Stepping Down Crypto billionaire Bankman – Fried eyeing bid for Celsius assets - BBG First resistance sited at 21k support now see at 18k 20 Day VWAP is bullish, 5 Day bullish

from Tickmill Expert Blog - Forex Traders Blog https://www.tickmill.com/blog/daily-market-outlook-september-28-2022"

via IFTTT

from Tickmill Expert Blog - Forex Traders Blog https://www.tickmill.com/blog/daily-market-outlook-september-28-2022"

via IFTTT

Market Update – September 28 – Renewed selling

- USDIndex – breaks range and tops at 114.63. Economic data on confidence, durables, home sales, and the Richmond Fed index were stronger than expected, while home prices declined and broke a long string of gains.

- Yields: A tweet from DoubleLine Capital’s Gundlach that he was buying Treasuries provided some support along with dip-buying and safe haven demand. The 10-year Treasury yield ended over 5 bps higher, testing 3.99% after having dropped over 10 bps to a low of 3.797%.

- GBP in a renewed selling, UK bonds sold off sharply yesterday a third day of turbulent trading, Yields on US bonds higher and US stocks to the lowest level since 2020. 10-year gilt on Tuesday rose 26% to hit a 14-year high of 4.5% after the Bank of England’s chief economist Huw Pill said the loosening of fiscal policy announced last week would “require a significant monetary response”.

- Kwarteng met the heads of companies including Aviva, Legal & General, Royal London, BlackRock, Schroders and Fidelity, to reassure them that his economic strategy would work after days of turmoil in financial markets. Later spoke to Conservative MPs to calm fears that the government had lost control of the economic situation.

-

IMF criticise Britain’s new economic strategy, saying the proposals are likely to increase inequality. Moody’s warned that unfunded tax cuts were credit negative.

- EUR – fresh low at 0.9540.

- JPY traded at 144.70.

- Stocks: closed mixed with the US100 managing a 0.25% gain, while the US30 declined -0.42%, with the US500 sliding -0.2% to 3647.

- USOil steady at $77 .The energy crisis in Europe intensified as European authorities investigated what Germany, Denmark and Sweden said were attacks which had caused major leaks into the Baltic Sea from two Russian gas pipelines.

- Gold – drifted to $1619.97.

- BTC – slide back to $18K area, as stocks fell deeper into a bear market. Ether was also down by less than 1%. – “crypto winter” ?

Biggest FX Mover @ (06:30 GMT) AUDJPY (-0.77%) extemds outside daily BB. Intraday fast MAs aligning lower, MACD histogram & signal line are negative, RSI at 23, H1 ATR 0.218, Daily ATR 1.166.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

from HF Analysis /519414/

via IFTTT

Tuesday, September 27, 2022

The best student bank accounts

As we approach the start of an academic year, Ruth Jackson-Kirby rounds up what you should look for when choosing a student bank account and outlines some of the best deals.

from Moneyweek RSS Feed https://moneyweek.com/personal-finance/605210/the-best-student-bank-accounts

via IFTTT

from Moneyweek RSS Feed https://moneyweek.com/personal-finance/605210/the-best-student-bank-accounts

via IFTTT

Technical update – Sterling Grosses

Sterling has seen sharp falls in most pairs, some with runs of over 1000 pips from their highs and some with 800 pips today alone. This is in the wake of the mini-budget reported on Friday, which is casting doubt on the UK’s economic future and causing investors to question the decisions of its new government and the BoE.

Today, the country’s largest mortgage lenders have suspended and withdrawn new mortgage deals thanks to rising costs for lenders due to the new tax cut announced last week by the new finance minister, Kwasi Kwarteng, which in turn pushed bond yields higher.

This is in addition to several disappointing economic data which you can read in this previously published article.

EURGBP – $0.8944

The EURGBP price has soared from the lows of 0.8686; after being range bound for several days in a bullish channel, it rose more than 500 pips and the price made a high of 0.9254, testing the Sep 2020 highs. The price has trimmed gains testing the 61.8% Fibo level at 0.8906 but closing just below the psychological level of 0.9000 which will act as a buy or sell signal.

The next highs are the March 2020 highs at 0.9496 followed by the October 2016 highs. Supports are at the 20-period SMA (H4) at 0.8850 along with the broken channel guideline, followed by the 88.6-78.6 range at 0.8753-0.8809 along with the 50-period SMA (H4) at 0.8785. Lows at 0.8689. 200-period SMA (H4) is at 0.8602. RSI at 55.76 after reaching 89.23.

GBPUSD – $1.0773

The GBPUSD price has accelerated its fall from the highs of 1.1737, dropping over 1400 pips and breaking the modern day lows of February 1985 at 1.0520, and trading at levels not seen since the Bretton Woods monetary system was abandoned in February 1972, making new all time lows at 1.0333.

Resistance is at the 38.2% Fibo level at 1.0869, followed by a range from the 20-period H4 SMA which crossed the 1.10 level to the 50% Fib. at 1.1035 and then the 61.8% Fibo along with the psychological level at 1.1201 and the 50-period SMA at 1.1239. Regarding supports, there is only the current historical low which is likely to be broken and the psychological levels up to parity at 1.00 which is the key level in focus. RSI at 39.87 after being oversold.

GBPAUD – $1.6610

The GBPAUD price fell sharply lower after ranging from 1.7100-1.6895, retracing more than 1000 pips lower and making lows at 1.5915, prices not seen since March 2017.

Current resistances are at the 61.8% Fibo level at 1.6650, the 20-period SMA at 1.6746, followed by the 88.6% Fibo level at 1.6968 near the base of the range and the psychological level of 1.7000. Support levels after the current range of 1.5915-1.6000 are at 2016 lows at 1.5361, 2013 lows at 1.4379, 1985 lows at 1.3606 and historical lows are at 1.2781 from 1976. RSI at 44.40 flat after recovering oversold.

GBPCAD – $1.4742

The GBPCAD price made new all time lows at 1.4075 after falling more than 1200 pips from multi-day range highs at 1.5297, breaking past all time lows at 1.4559 of February 1985. The price has recovered the historical lows of 1985 and has resistance at the 61.8% Fibo at 1.4831. The 20-period SMA is at 1.4905, the base of the range at the 78.6% Fibo is at 1.5000-1.5036.

GBPJPY – $155.574

The GBPJPY price accelerated its fall from 167.15 highs to 148.92 lows, a price not seen since July 2021. The price has recovered from the 150.00-155.00 level and remains below the 38.2% Fibo at 155.88. Resistance is at the 20-period SMA at 157.36, the 50% Fibo at 158.03, and the psychological level of 160.00. Support is at 148.92-150.00 area. RSI flat at 41.91 after recovering oversold.

GBPNZD – $1.8960

The GBPNZD price was in a bullish channel since early September where it made a high at 1.9380 but failed to hold the level and fell sharply over 1200 pips to a low at 1.8158 (2018 lows), but trimmed losses at the close of today’s session. Resistances are at the psychological level of 1.9000 which can be used as a watershed between buys and sells, followed by the 20-, 100- and 200-period SMA.

GBPCHF – $1.0667

The GBPCHF price accelerated its downtrend for the year and fell over 900 pips breaking last year’s lows at 1.1118 and making new lows at 1.0179, prices not seen since November 1976.

Resistance is at the 61.8% Fibo and 20-period SMA at 1.0777, followed by the 50-period SMA and 78.6 Fib. at 1.09110-1.093397 and the psychological 1.1000 level. The break of the latter leaves no support apart from today’s new low and the 1.0500 level.

Click here to access our Economic Calendar

Aldo Zapien

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

from HF Analysis /519607/

via IFTTT

The IndeX Files 27-09-2022

Equities Attempting Recovery Following Heavy Monday LossesGlobal equities benchmarks have seen a mixed start to the week with most indices finding their feet today after heavy selling across Monday’s trading. The ongoing rise in USD on the back of last week’s FOMC meeting has had a heavy downward impact on equities prices. With the Fed acknowledging that elevated inflation is here to stay for longer than first thought, the market has done away with any near-term idea of a Fed-pivot. Instead, hawkish expectations have become entrenched with many players now suggesting .75% hikes will be the new .25% hikes as the Fed battles inflation.With a slew of central banks having hiked rates in recent weeks, global bond yields have been on the rise, adding further pressure to equities markets. Recessionary fears have taken centre stage in recent weeks. Price action in GBP over the last two trading days highlights the level of nerves in the market currently. While equities prices are stabilising a little today, amidst a softer start for the US Dollar, downside risks remain key. Powell speaks later today and his comments have the potential to turn equities lower again if the Fed chair is seen adding further details to his concern over the inflation outlook. The latest US consumer confidence report due today is also likely to add to bearish sentiment for equities traders while traders will also be watching the latest durable goods numberTechnical ViewsDAXThe breakdown below the 12462.59 level, marking new lows for the year, is a significant development for the market. While below this level, and with MACD and RSI bearish, the focus is on a further push lower towards the 11590.13 level next. Back above, and 13067.45 is the first resistance for bulls.S&P 500The breakdown below the 3910.00 level in the S&P has seen the index plunging back towards the yearly lows around 3647.00. While bulls can defend this level, there is potential for a rebound. However, price action remains a heavy and a break down towards new lows and next support at 3534.75 is the big risk.FTSEThe sell of fin the FTSE has seen the market hurtling down towards the 6994.2 level. Price briefly pierced below the level before trading back above and, while this support holds, a rebound to 7213.9 is viable. Should we break lower, however, in line with bearish MACD and RSI, the 6827.3 level and bear channel lows, is the next support area to watch.NIKKEIThe sell-off in the Nikkei has seen the market breaking through the 27422.9 level and trading down o test the rising trend line from year to date lows and the 26246 level support. While this level is holding for now, bearish MACD and RSI suggest risks of a further move towards 25500.5 next.

from Tickmill Expert Blog - Forex Traders Blog https://www.tickmill.com/blog/the-index-files-27-09-2022"

via IFTTT

from Tickmill Expert Blog - Forex Traders Blog https://www.tickmill.com/blog/the-index-files-27-09-2022"

via IFTTT

Subscribe to:

Comments (Atom)

-

The new strain of covid found in South Africa could disrupt plans by governments and central banks to rebuild economies. Financial markets a...

-

Fidelity “FIS” is a global financial services technology company and a leader in providing technology solutions to merchants, banks and cap...

-

Asian Equities Sink on Covid FearsIt’s been a mixed start to the week for global equities benchmarks with US and European asset markets rema...