Dax H1 is at Pivot after breaking symmetrical triangle where we could potentially see a drop towards the 1st support level, in-line with 50% Fibonacci retracement and 78.6% Fibonacci extension. If price bounce from the pivot, we may see it swing towards 1st resistance, in line with 50% and 61.8% Fibonacci retracement and horizontal overlap resistance

from Tickmill Expert Blog - Forex Traders Blog https://www.tickmill.com/blog/dax-h1-is-at-pivot-potential-for-drop"

via IFTTT

Tuesday, June 29, 2021

Nikkei approaching support, potential for reversal

Nikkei is approaching key graphical swing low support at our Pivot. We see a medium probability for an intraday bounce above our pivot towards descending trendline resistance, moving average resistance and 61.8% Fibonacci retracement at our 1st resistance. Stochastic is also reacting above support where price bounced in the past

from Tickmill Expert Blog - Forex Traders Blog https://www.tickmill.com/blog/nikkei-approaching-support-potential-for-reversal"

via IFTTT

from Tickmill Expert Blog - Forex Traders Blog https://www.tickmill.com/blog/nikkei-approaching-support-potential-for-reversal"

via IFTTT

EURUSD, H1, approaching pivot, potential for bounce

EURUSD H1 is approaching pivot, in-line with 61.8% Fibonacci retracement and 161.8% Fibonacci extension. We may potentially see a bounce towards the 1st resistance level, in-line with 38.2% and 50% Fibonacci retracement and horizontal overlap resistance. If price breaks the pivot, we may see it swing towards 1st support, in-line with 78.6% Fibonacci retracement and 200% Fibonacci extension.

from Tickmill Expert Blog - Forex Traders Blog https://www.tickmill.com/blog/eurusd-h1-approaching-pivot-potential-for-bounce"

via IFTTT

from Tickmill Expert Blog - Forex Traders Blog https://www.tickmill.com/blog/eurusd-h1-approaching-pivot-potential-for-bounce"

via IFTTT

BTCUSD reversing from pivot, potential for further downside

Prices have reversed from pivot level in line with 161.8% Fibonacci extension and horizontal swing high resistance. Prices might push down towards horizontal overlap support in line with 61.8% Fibonacci retracement and 61.8% Fibonacci extension. Stochastics is also at resistance, potential for reversal. If prices continue to push up, prices might face resistance from horizontal swing high resistance in line with 127.2% Fibonacci retracement and 100% Fibonacci extension.

from Tickmill Expert Blog - Forex Traders Blog https://www.tickmill.com/blog/btcusd-reversing-from-pivot-potential-for-further-downside"

via IFTTT

from Tickmill Expert Blog - Forex Traders Blog https://www.tickmill.com/blog/btcusd-reversing-from-pivot-potential-for-further-downside"

via IFTTT

What will pop the UK's house price bubble?

Annual house price growth hit 13.4% last month, according to Nationwide figures.

That’s a horrible statistic for any would-be first-time buyer to read, and if you’re in that position, I sympathise.

I’d like to be able to tell you that relief is on the horizon.

Unfortunately, I don’t think it is.

The end of the stamp duty holiday isn’t going to bring any relief

The latest surge in annual house price growth – to the highest level since November 2004, slap bang in the middle of the last house price bubble – is admittedly not quite as wild as it looks.

June last year was, as Nationwide’s chief economist Robert Gardner puts it, “unusually weak”. House prices actually dipped that month, because we were all in ultra-lockdown as opposed to the rolling pseudo-lockdown we’re stuck in to various extents right now.

There were no vaccines then. Lots of people thought there wouldn’t be vaccines for at least five years. And back then, some of us even imagined that house prices might drop because of the pandemic.

Needless to say, that’s not what happened. Prices have risen every month in the past five, according to Nationwide.

So while the 13.4% rise in prices has been a little exaggerated due to the “base” effect of being by comparison to a very weak month last year, that’s really very little consolation for anyone who doesn’t think that it’s healthy economically or socially for the cost of a basic human need to be rising at such a rapid rate.

Is anything going to change this any time soon? The most obvious crumb of comfort on the horizon is the end of the stamp duty holiday (though it’s already ended in Scotland), which many blame for pouring fuel on the fire.

UK house price indices

It’s almost certainly true that the stamp duty holiday has pulled forward transactions that would otherwise have happened later in the year. That in turn means an artificial surge in demand without a corresponding artificial surge in supply.

Also sellers aren’t daft. They know a stamp duty holiday means they can bump their own sale price up at least a little. If the buyer doesn’t have to pay a big cash lump sum in stamp duty, it means they can afford to borrow more to buy the actual house. Hence at least some if not all of the stamp duty savings accrue to the sellers and their agents, not to the buyer.

So there’s no doubt that a stamp duty holiday is going to boost house prices, all else being equal.

So you might be hoping that as it ends or becomes less generous (depending on which part of the UK you are in), that prices might calm down a little.

What will end the house price bubble – inflation

Unfortunately, the end of the stamp duty holiday is not going to put an end to all this. As Andrew Wishart of Capital Economics points out: “The tax break is just one of a laundry list of factors behind the surge in house prices over the past year.”

What do those include? We’ve been through it before but the list includes low interest rates; rising mortgage availability; a pent-up desire to move after the lockdown; and an added desire to move as people adjust to new working patterns.

Now the last two things are possibly temporary factors. But I can see it taking a while to settle down. And in any case, they’re not really the fundamental driving force behind the rising prices.

Yes, you’ve arguably got an outflow of money from expensive (ie commuter belt) areas to less expensive (ie previously non-commuter belt) ones which probably means you have a wave of slightly less price sensitive buyers than before.

But the real issue – as always with houses – is the supply of credit to the market. And that shows no sign of seizing up.

Wishart argues that house prices will likely “moderate” rather than crash, and on an annualised basis that’s probably reasonable, given that for the rest of the year, the comparators will be tougher. (In other words, the year-on-year figure won’t be compared with weak months).

Also it’s worth noting that affordability – as measured by the Nationwide – is now very close to where it was at the peak of the last bubble in 2007. Does that mean the bubble will pop?

As far as I can see, there’s only one way it happens. I don’t think we’re going to get a repeat of 2008 anytime soon.

So until inflation takes off and the Bank of England and credit markets respond by tightening the cost of borrowing (Andy Haldane had a bit to say about this in the latest MoneyWeek podcast), it’s hard to see house prices coming down.

However, it does mean that until then, we’re going to be stuck with this social and economic problem which is a lack of affordable housing.

How will that resolve itself? I’d expect to see more pressure to build more homes. That might help at the margins in some areas, but it doesn’t address the credit issue.

It might also increase the pressure on wages to go up, which is inflationary in itself.

The government might even throw more fuel on the fire at some point by coming up with more first-time buyer schemes that are just taxpayer-backed subsidies for house builders or home sellers.

In the meantime, if you’re looking to buy a house, I can only refer you to this article in which I explained that worrying about the big picture outlook is usually a waste of time. If you want to buy a house to live in, it’s your personal circumstances that really matter.

from Moneyweek RSS Feed https://moneyweek.com/investments/property/603475/what-will-pop-the-uk-house-price-bubble

via IFTTT

Daily Market Outlook, June 29, 2021

Daily Market Outlook, June 29, 2021 Overnight Headlines Asian equity markets are mostly down this morning, following declines in Europe and a mixed performance in the US yesterday. Concerns about a renewed rise in Covid-19 cases has been cited as a reason. UK daily coronavirus cases climbed to their highest since the end of January yesterday. Nevertheless, PM Johnson said that 19th July would "very likely" remain the date for ending Covid-19 restrictions in England. Reports suggest that agreement for general UK travel to the US is now unlikely before September. Some EU countries have also tightened restrictions on travel from the UK. Today’s Bank of England money supply and bank lending data for May will give a timely indication on the strength of the UK’s buoyant housing market. The extension of the stamp duty holiday in March’s budget seems to have given the market a further lift. Nevertheless, the level of mortgage transactions is still expected to be down slightly from April. In contrast, bank lending secured on dwellings, which was surprisingly weak in April, is forecast to have picked up. Other lending measures will provide additional insight into the strength of consumer and investment spending. Today’s June CPI data for Spain and Germany will give some insight into tomorrow’s update for the Eurozone as a whole. Annual inflation rates have gone up in both countries this year, primarily because of the rise in the oil price. Expectations for this month are that annual inflation will hold at 2.4% in Spain but fall modestly in Germany to 2.1% from 2.4% in May. That would be consistent with a small decline in Eurozone ‘headline’ inflation. Also to be released are the European Commission’s measures of economic confidence that are thought likely to provide further evidence of a second-quarter rebound in economic activity. In the US, the Conference Board’s consumer confidence measure slipped in May for the first time in six months, possibly due to concerns about rising inflation. However other consumer sentiment measures point to a modest rebound in June. The Lloyds Business Barometer for the UK rose for the fourth consecutive month in May to its highest level in three years, reflecting an improvement in businesses’ own prospects and their feelings about the wider economy. However, as June has seen an acceleration in Covid-19 cases and the decision not to end all restrictions, it is uncertain whether the latest update, which is out early tomorrow, will post another rise. It will also provide further information on the state of the labour market and price pressures.G10 FX Options Expiries for 10AM New York Cut(Hedging effect can often draw spot toward strikes pre expiry if nearby)EUR/USD 1.1900-10 (625M), 1.1985-90 (426M), 1.2050 (375M)USD/JPY 109.35-45 (1.2BLN), 110.10-15 (680M), 110.85 (465M)111.00 (430M), 112.00 (1.228BLN). EUR/JPY 132.35 (240M)EUR/GBP 0.8500 (360M). AUD/JPY 84.35 (342M)AUD/USD 0.7600 (302M). NZD/USD 0.7260 (720M)USD/CHF 0.9195-00 (340M). USD/CAD 1.2300-10 (570M)Technical & Trade ViewsEURUSD Bias: Bearish below 1.21 Bullish aboveSlips as USD and JPY firm in risk off session • EUR/USD opened 0.11% lower at 1.1928 after a quiet US session • After trading at 1.1929 it edged lower with EUR/JPY selling adding weight • Mood in Asia was risk-off with most equity markets easing • EUR/USD traded down to 11.1907 and is around 1.1910 into the afternoon • EUR/USD bids are tipped ahead of 1.1900 with support at 1.18845/50 • Sellers are lined up around 1.1975 with resistance at 38.2 fibo at 1.2007 • Sentiment is mildly bearish ahead of US non-farm payrolls on FridayGBPUSD Bias: Bearish below 1.4080 Bullish above.Soft, reflecting the negative technical outlook • -0.1% in a 1.3859-1.3878 range – decent flow once Asia fully opened • Negative sterling signals ahead of 'freedom day' • Charts; daily momentum studies, 5, 10 & 21 daily moving averages fall • 21 day Bollinger bands slide – bearish setup suggests further losses • 10 DMA capped repeatedly, now comes in at 1.3908 – pivotal resistance • Downtrend targets a test of 1.3756, 61.8% of the 2021 rise • 1.3786 June low and 1.3908, 10 DMA initial support and resistance Negative sterling signals ahead of 'freedom day' While sterling has been in a holding pattern for a week, recent topside failures leave the daily charts showing a significant bearish bias ahead of Britain's July 19 'freedom day'. Political controversy continues in the UK after the health minister resigned over the weekend. His replacement Sajid Javid strongly believes the battle between vaccination and the spread of COVID-19 is close to being won, with 22,868 new cases on Monday and only 3 deaths . Javid and Prime Minister Boris Johnson expect 'freedom day' to become a reality on July 19, as the UK fully reopens and begins what will become a new 'normal' life . If reopening is successful, it will be sterling-positive longer term. Short term the technical picture has developed a decidedly negative look. Daily momentum studies, 5, 10 and 21 daily moving averages all head south, while the 21-day Bollinger bands slide, which is a strong bearish trending setup. The falling 10-day moving average capped on three of the last four days, and now comes in at 1.3909. A close above 1.3909 would undermine the downside bias, and a close above 1.4018/28, 50% of the June fall and 21 DMA, would end it. The downtrend targets a test of 1.3756, 61.8% of the 2021 rise, then the 1.3669 April lowUSDJPY Bias: Bullish above 108 targeting 112JPY crosses off again after Tokyo fix • USD/JPY, JPY crosses peak out into today's Tokyo fix, off post-fix • This the pattern recently especially in USD/JPY, 110.64 to 110.46 EBS • USD/JPY downside limited though, bids still sub-110.50, trail down • Massive, $1.1 bln in option expiries today down between 110.00-15 • Upside just as limited ahead of 111.00, $465 mln expiries at 110.85 • Tech support at now flat 110.41 Ichi daily tenkan, kijun 109.83 below • US yields soggy, Treasury 10s @1.477%, risk-off, Nikkei -0.9% @28,791 • EUR/JPY 132.92 to 131.63, GBP/JPY 153.62 to 153.09, AUD/JPY 83.72 to 83.40Options to help contain USD/JPY into U.S. jobs data Massive USD/JPY option expiries near current spot levels are likely to help contain USD/JPY price action into Friday's keenly anticipated U.S. non-farm payrolls data. June non-farm payrolls are expected to rise by 690,000 according to a Reuters poll (May +559,000) and the unemployment rate to tick down to 5.7% from 5.8% in May. Massive option expiries have already been evident recently, including $1.3 billion at 111.00 on Friday and $1.4 billion at 110.50 on Monday. Tuesday sees $1.1 billion between 110.00-15 strikes and Wednesday $1.45 billion between 110.20-25, $1.3 billion at 110.50 and $1.3 billion between 110.70-75. Friday also sees large strikes on 110 and $1.7 billion at 111.00.All of these strikes will work to keep USD/JPY in a core 110.50-111.00 or tad wider 110.00-111.50 range until the key jobs report. Moves within these ranges will be driven by U.S. yields, which have seen very choppy trading of late, surging Monday only to fall off sharply later in the day as the S&P 500 index and Nasdaq hit fresh record highsAUDUSD Bias: Bearish below .7790 bullish aboveDrifts lower in risk-off Asian session • AUD/USD opened 0.32% lower at 0.7565 as USD firmed against risk currencies • After trading 0.7570 it came under pressure as Asian shares moved lower • Mood was risk-off with E-minis easing 0.16% and key commodities slipping • AUD/USD traded down to 0.7550 and is at the lows into the afternoon • Buyers tipped ahead of 0.7500 with support at double-bottom at 0.7478 • AUD/USD sellers 0.7600/10 with resistance at 38.2 fibo at 0.7635 • Sentiment mildly bearish, but range likely to hold ahead of Friday's US jobs • COVID-related lockdowns in Australia may limit upside for now

from Tickmill Expert Blog - Forex Traders Blog https://www.tickmill.com/blog/daily-market-outlook-june-29-2021"

via IFTTT

from Tickmill Expert Blog - Forex Traders Blog https://www.tickmill.com/blog/daily-market-outlook-june-29-2021"

via IFTTT

Wedding costs: how to cut the big bill for your big day

The 30-person cap on marriage ceremonies in England and Wales was scrapped this week. But weddings are still puritanical affairs, with tight curbs on singing and dancing. Social distancing must be respected, which can limit guest numbers. In Scotland hard limits are still in place and depend on the “protection level” in force in the local area. The removal of the 30-person cap is a relief to couples, who have avoided the heart-breaking prospect of having to disinvite people over the guest limit. But some will still postpone the big day. The new rules are “like giving you a trifle and not putting the jelly in it”, Kathy Leather from Malvern, who with her partner has decided to postpone her wedding, tells the BBC. “You can’t have a celebration without chatting and dancing and singing”. It’s “a lot of money to not do what you want to do”.

When it comes to getting money back, weddings cancelled because of lockdowns are straightforward: guidance from the Competition and Markets Authority (CMA) says that “the starting point under the law is that the consumer should be offered a full refund”. The current restrictions make things more complicated. What if your wedding can go ahead, but the rules mean it falls far short of what you had planned?

Helen Saxon and Jenny Keefe on Moneysavingexpert.com say the first step is to try to sort things out amicably with the venue and suppliers (keep in mind that Covid-19 has devastated their industry). It may be possible to negotiate reductions on items such as catering charges for a scaled-back ceremony. Also investigate whether your wedding insurance or card chargebacks offer any protection.

Would you be within your rights to cancel? The key legal concept is that of “frustration”, defined by the CMA as applying when a contract can’t be performed or “performance would be radically different to what was agreed”. Frustration brings the contract to an end. Not all changes count as frustration. A wedding set to go ahead “at the agreed venue, with catering and a reception mainly as agreed, for a substantial majority of the agreed number of guests” is unlikely to be judged frustrated in court.

Cancelling is expensive: for example, Sarah Rainey in the Daily Mail reports that one Hertfordshire couple faces losing a £4,000 venue deposit and another £5,770 on deposits paid to other suppliers in the event of cancellation.

That said, deposit money is not necessarily lost. Contract terms such as “non-refundable deposit” carry little legal weight. Venues are entitled to subtract reasonable costs from refunds but these “must reflect what it is actually losing as a result of the cancellation”, says the CMA. That applies to things such as meal tastings, flowers and staff hours worked on preparation. The later you cancel the higher these costs are likely to climb. Consumers who cancel an event that could have gone ahead “should not face disproportionately high charges for ending the contract”.

Hail the micro-wedding

Will scaled-back weddings last beyond the pandemic? Soaring property prices are changing people’s priorities. A Halifax survey reports that 62% of engaged British couples “would consider reallocating their wedding budget towards a deposit for a house”. The trend even has a name. In America the “micro-wedding”, with guest counts as low as 25, is reportedly gaining popularity. Lower guest counts cut costs and allow more flexibility in venue choice.

“I always cry at weddings,” says Linda Kelsey in the Daily Mail. Why? “The mad scale and the crazy cost – £32,000 on average for a 100-plus guest list… I sincerely hope that dramatically downsized weddings are here to stay.”

from Moneyweek RSS Feed https://moneyweek.com/personal-finance/603444/wedding-costs-how-to-cut-the-big-bill-for-your-big-day

via IFTTT

Private equity isn’t evil, it’s just doing what traditional investors should be doing

Fund managers in the UK are a bit upset. US private equity group Clayton, Dubilier & Rice made a 230p per share offer for supermarket chain Wm Morrison. The board rejected the bid on the grounds that it “significantly undervalued” the firm. The market seemed to agree, pushing the share price of Morrisons up to 240p.

You might ask what the problem is here. Morrisons was trading at 178p. Now it’s trading at 233p. That ought to please most investors.

Instead there is discontent, and it has two causes. The first is that not everyone considers private equity firms, with their reputation for asset stripping and financial engineering, to be good stewards of long-established companies. The second is that Clayton, Dubilier & Rice isn’t offering enough for Morrisons.

This first argument isn’t entirely fair. While private equity often shows a tendency to over-leverage and underinvest, there is nothing intrinsically good or bad about private equity when it comes to management. It is just a different corporate governance model, the success or not of which will depend, as with listed companies, on the competence and creativity of the managers.

The trouble with private equity is about shareholder democracy

If there is a problem, it is more one of transparency and participation. If private equity ends up owning the UK supermarket sector, the shelves will surely be as full as ever, but we may lose a say over what is on those shelves.

In March, ShareAction, a UK pressure group, forced Tesco to put a resolution to shareholders at its next annual meeting that would – if passed – require it to disclose targets and progress around encouraging shoppers to opt for fewer fatty, salty and sugary foods. You might disapprove of this, or not. There are upsides, including perhaps less obesity, and downsides, insofar as less processed food sold might mean lower margins.

The essential point is that shareholders can make a difference on matters of this kind, and not only at AGMs. After the forcing of the resolution, Tesco pledged to aim to lift the proportion of “healthy products” it sells to 65% of total sales by 2025. The more companies think votes will be used, the more they will react to them (this has been a record year for ESG resolutions at listed companies). Private equity might say they are the perfect shareholder democracy – one shareholder, one vote. I’d say democracy works better when it’s not an elite sport.

We should be buying these undervalued companies ourselves

On to the money. If 230p isn’t enough to pay for Morrisons, you might ask why investors were perfectly happy to see it trading at 178p in the first place. Might it be that not enough traditional fund managers were holding many of the shares they now consider to have been much too cheap last week?

Traditional fund managers like to think of themselves as a little contrarian – or at least to tell everyone that’s how they think of themselves. This is usually nonsense, something pretty firmly proven by not just the Morrison offer but others in the UK market this year. Private equity firms have now bid for 13 UK listed businesses since 1 January. Why? Because that’s where the value is, the value traditional fund managers have left on the table.

The private equity business is awash with cash. It’s gone from strength to strength over the past decade thanks to the popular, but as yet unproven, belief that it offers better long-term returns than listed markets. By the beginning of this year McKinsey reckons the sector was worth about $7.3trn.

It’s an area conventional fund management companies have been clamouring to get into. Ask a fund manager what his plans are and odds are he’ll say he intends to buy private companies – because that’s where the growth is. But it turns out that, while traditional fund managers have been eyeing up the cool growth stuff private equity is supposed to buy, private equity has begun to eye up the stuff the traditional fund managers are supposed to buy.

With everyone wanting to be in the game, the multiples paid globally for private companies have hit all-time highs. But thanks to their unexciting workaday characteristics, those paid for listed UK companies have not. Before Morrisons announced the bid, its share price was down 9% over a year.

Fund managers have only themselves to blame

It’s not the only neglected stock out there. Shares in the UK’s big oil companies are 30% or more below where they were when the oil price was last $70 a barrel in 2018. BT Group is down 47% over the past five years – which is probably why French billionaire Patrick Drahi stepped in to buy 12.1% of it.

Traditional fund managers are culpable. They’ve been so busy agitating to get a piece of the stuff that has performed well in the past that, a few dedicated income funds aside, they’ve started missing obvious opportunities – one being the cheapness of the UK market. You can argue that a company such as Morrisons is worth more under private equity owners than on the listed market simply because the former can do clever things such as sale and lease back the firm’s shops.

But there is no reason why ordinary fund managers can’t push for the same measures. If they did their jobs properly, there would be no cheap listed UK companies for private equity companies to snap up – they would already have been bid up to something close to fair value. No wonder fund managers are upset.

• This article was first published in the Financial Times

from Moneyweek RSS Feed https://moneyweek.com/investments/stockmarkets/uk-stockmarkets/603471/private-equity-isnt-evil-its-just-doing-what

via IFTTT

Market Update – June 29 – Valuations, End of Quarter, Fear

Sentiment remains cautious and stocks under pressure, but Treasury yields tumbled lower on the day, recovering all of last week’s losses, and then some. The 10- and 30-year yields fell over 5 bps to the 1.4698% and 2.0857% areas, respectively, on the day, with the break in key technical levels of 1.50% and 2.10% supporting the richening. Concern about the spread of the more infectious Delta variant of the virus is weighing on confidence as governments try to limit the impact.

Equities remain mixed, with the USA100 holding in record territory, and keeping the bulk of its gains. The USA500 continues to idle on either side of unchanged, while the USA30 underperforms, losing over 200 points early on, then recovering slightly in afternoon trade. The USA30 components Chevron off over -3% as oil prices faded, while Boeing shed -3% after being told certification of its new long range aircraft would not come until at least 2023. The energy and financial sectors were the biggest laggards, while utilities and tech paced winning sectors.

Valuations remain a question for further stock market gains, with the USA500 P/E ration this highest in over 10-years.

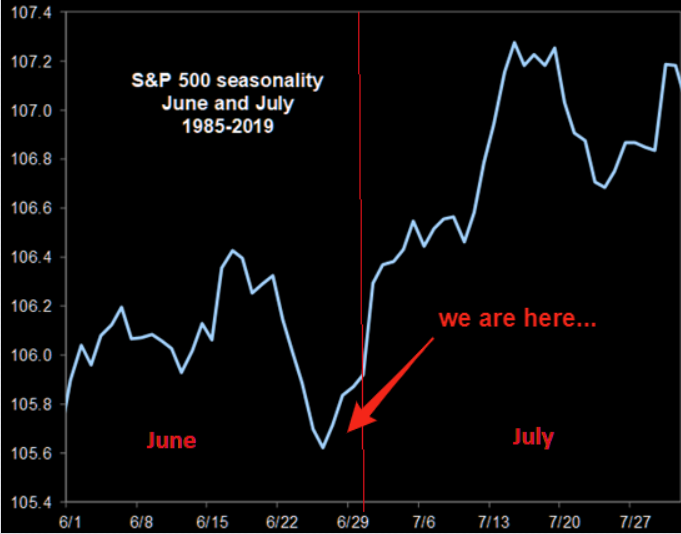

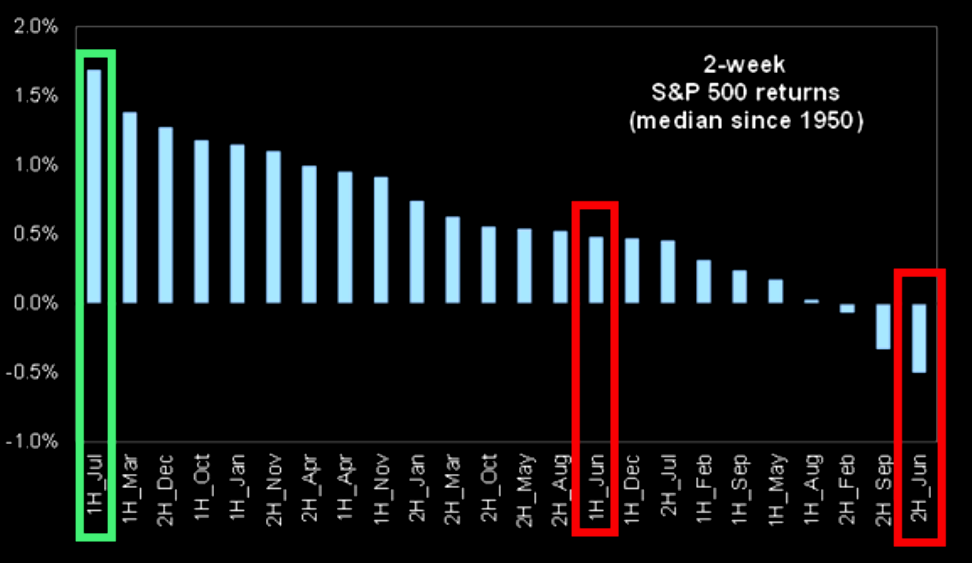

The charts that matter

Significant long-term charts with historical price data back to 1950, remains very powerful and important.

- The 2 first weeks of July are the best weeks of the year

- “we are here” – S&P is just starting if you look at the seasonality pattern since 1985

- After the 2 first weeks of July, SPX and Russell tend to “chill”, while NDX continues moving higher, but above all, note the NDX pattern starting now

- Exposure in FAANMGs is close to record lows

- Tech’s range break out has been extremely powerful, and the candle today shows just how strong this momentum remains

Forex Market: EURUSD is little changed at 1.1907. The Australia, NZ dollars weaken for second day on low risk appetiter, USDJPY steadied to 110.10-60 while the EUR steadied between 1.1920-1.1970 for a 5th day. The Pound strengthened further with cable to 1.3857. Gold prices edged lower as USDIndex hovers below 2-month high.

USOIL slid to 3-session lows of $72.63 after printing new trend highs of $74.45 in Asia. The move lower was linked to concerns over rising Covid cases in many parts of Asia, including Thailand, Malaysia and Indonesia, which prompted some profit taking from 32-month highs. In addition, long positions may be cut ahead of the OPEC+ meeting on Thursday, where expectations are for an announced production increase, beginning in August.

Tuesday’s Calendar – Data releases today include Eurozone ESI economic confidence, German June HICP, UK lending data, while US Consumer confidence is also due, but virus headlines will likely dominate.

Significant FX Mover @ (06:30 GMT) USA30(+0.34%) dipped by more than 0.44% from 34,525 to 34,172 low. Faster MAs and RSI are currently flattened,while MACD signal line and histogram are negatively confugured , all suggesting that in the short term decline ran out of steam and the asset is consolidating fo the time being.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

from HF Analysis /248416/

via IFTTT

US100 & US500 at all-time highs, Facebook joins the $1 trillion club

The US500 (S&P500) and US100 (NASDAQ) futures indexes traded at historical highs on Monday following positive market sentiment. Facebook shares joining the $1 trillion club gave support to the US100 index following a district court decision dismissing the FTC’s antitrust case against Facebook (up 4.18%). Other technology stocks such as Intel (up 2.81%), Microsoft (up 1.4%) and Apple (up 1.26%) also supported the rise of the US100 index.

The US500 index reached a high of 4281.44 points in late trading before declining slightly to 4277 before closing at new all-time highs at 4290.62 it closed with strong bullish momentum and remains above the MA-50 H1 level. It has remained traded in the ascending channel since June 21. The nearest support is at 4264 points.

Meanwhile, the US100 also set a record intra-day high when it reached 14,517.80 points before declining back to 14,492 and closing at the key psychological 14,500. The nearest support is well below at 14,420 points.

The strengthening of the US100 was supported by a surge in technology shares where Facebook managed to get a court order to set aside 2 complaints filed by prosecutors with respect to antitrust policies. The surge in Facebook shares pushed the company to be worth more than $1 trillion in market capitalization and join other big tech companies in the trillion+ company club. Facebook shares closed at historical highs at $355.37, an increase of more than 30% in 2021. 49 of the 58 analysts tracked by Bloomberg now place Facebook shares in the Buy category, 6 in the holdings category and only 3 place FB shares in the sell category.

Positive sentiment from the US close cooled in the Asian session, where Covid infections and continued lockdowns weighed on markets. The Nikkei JPY225 moved down to 28,689 to a 5-day low before recovering in late trading to close at 28,812 (-0.81%).

Click here to access our Economic Calendar

Tunku Ishak Al-Irsyad

Market Analyst

HF Educational Office – Malaysia

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

from HF Analysis /248401/

via IFTTT

Dollar Edges Higher; Asian Covid Cases Rise

from Forex News https://www.investing.com/news/forex-news/dollar-edges-higher-asian-covid-cases-rise-2544690

via IFTTT

Dollar Up, but Below Two-Month Highs as it Preps for June’s U.S. Job Report

from Forex News https://www.investing.com/news/forex-news/dollar-up-but-below-twomonth-highs-as-it-preps-for-junes-us-job-report-2544670

via IFTTT

USDJPY facing bearish pressure, possible drop

USDJPY is facing bearish pressure as it holds under moving average resistance. We could see further downside below Pivot, in line with 38.2% Fibonacci retracement, 50% Fibonacci extension and 127.2% Fibonacci extension, towards 1st Support, in line with 100% Fibonacci extension and horizontal swing low support.

from Tickmill Expert Blog - Forex Traders Blog https://www.tickmill.com/blog/usdjpy-facing-bearish-pressure-possible-drop"

via IFTTT

from Tickmill Expert Blog - Forex Traders Blog https://www.tickmill.com/blog/usdjpy-facing-bearish-pressure-possible-drop"

via IFTTT

Dollar bides time below two-month highs before payrolls test

from Forex News https://www.investing.com/news/economy/dollar-bides-time-below-twomonth-highs-before-payrolls-test-2544619

via IFTTT

Subscribe to:

Comments (Atom)

-

The new strain of covid found in South Africa could disrupt plans by governments and central banks to rebuild economies. Financial markets a...

-

Fidelity “FIS” is a global financial services technology company and a leader in providing technology solutions to merchants, banks and cap...

-

Asian Equities Sink on Covid FearsIt’s been a mixed start to the week for global equities benchmarks with US and European asset markets rema...